Annette Bui | Updated June 17, 2020, | Mortgage Programs 101

Contrary to what most consumers believe, the income calculation is much more conservative than you may realize because of Fannie Mae and Freddie Mac guidelines. When your income is salaried, and you have been with your current employer for two years then it is simple math. However, if your income is a base salary or hourly plus overtime, bonus, commission. Then the income is determined based on your past two-year history. Underwriters want to see your hours worked if you are hourly paid over the last two-year history. Generally speaking, if your overtime, bonus, commission, and hours worked are increasing in the last two years then they will average the amount including the year to date. However, if your income dropped recently due to fewer hours worked, less overtime availability then you may only be eligible to use the lower and most recent amount of earned income from overtime, bonus, commission. It all boils down to how your employer completes the verification of employment form and/or if you have the year-end paycheck stubs from the last two years to show the breakdown.

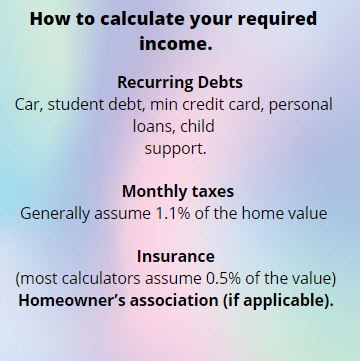

To alleviate questions, uncertainties as far as the income requirement based on your existing debts, mortgage balance, or desired loan for a purchase. Below is a cheat sheet:

Comments

Post a Comment